The holiday shopping season this year stands in stark contrast to 2021, a time when retailers, facing clogged supply chains and limited production of goods, struggled to keep their shelves stocked to meet the robust demand of shoppers flush with stimulus funds.

Fast forward to today: More than a year’s worth of rampant inflation has tempered consumer enthusiasm for spending, and supplies have loosened up to such a degree that merchandise is being discounted. Few items are in short supply, and finding those hot holiday items has become a relative breeze.

At least that’s the picture for physical goods. The story of consumer spending over the past year has been one of transition away from spending on goods like furniture, computers, cars and exercise equipment, as we were all hunkered down at home, and towards services such as travel, restaurant meals and entertainment, which had largely been restricted during the pandemic.

The latest retail sales report showed that spending fell in November by 0.6% over the month, the largest decline of the year and driven by a pullback in purchases of goods and by discounts offered by retailers hoping to clear overstocked shelves.

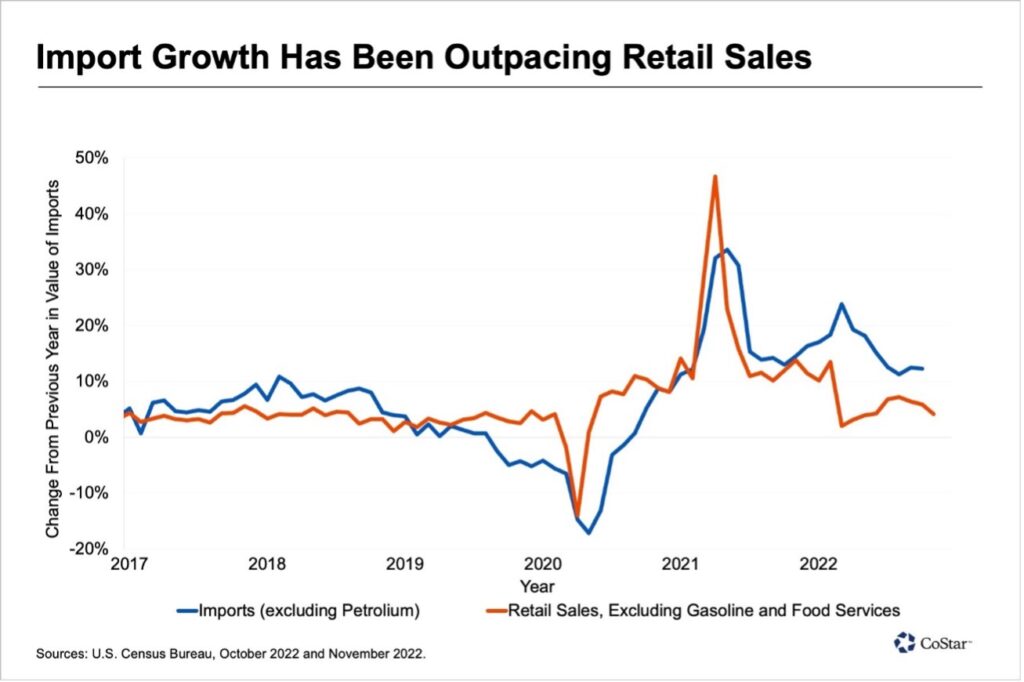

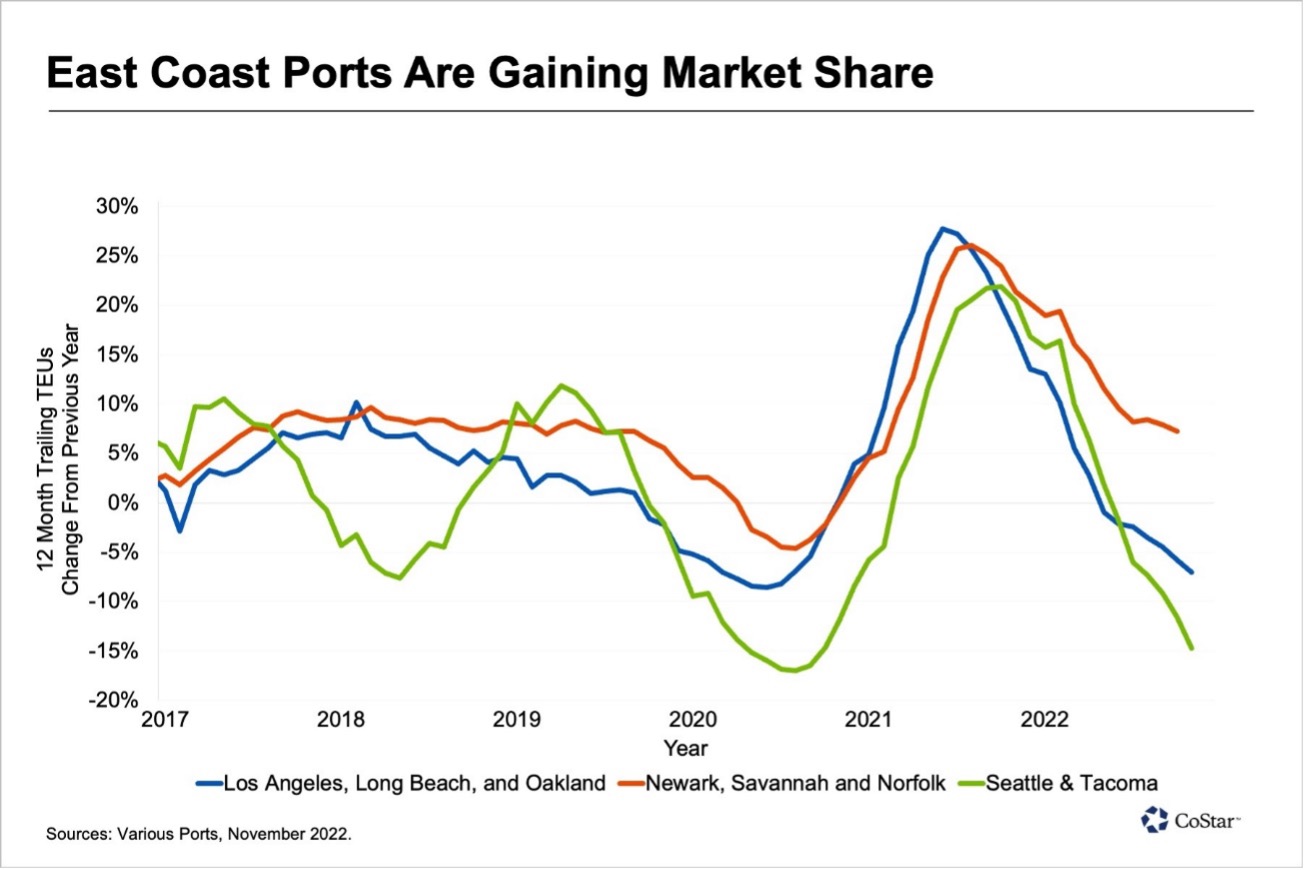

That same massive appetite for physical goods drove a good deal of the demand for industrial space over the past few years, as most goods were shipped from Asia and Europe to warehouses in the U.S. West and East. There is a strong correlation between imports (as measured by value) and retail sales, which lag imports by a month or two, so monitoring retail sales is a quick indicator into the future health of the industrial space market. However, that correlation has become less evident in recent months, suggesting that firms are struggling to adjust to the rapidly changing political and economic climate.

In 2018, soon after President Donald Trump imposed tariffs on China, import growth began to slow as more domestic product made its way into retail sales. Growth of both sales and imports diverged further at the onset of the pandemic as supply chains were disrupted and failed to keep up with the outsized demand for goods boosted by stimulus funds. Ships at ports waited for weeks to have their merchandise unloaded.